Capacitors in Renewable Energy Systems: Opportunities for Growth to 2030

02/13/2013 //

Introduction and Market Overview:

With global electricity needs expected to increase by 58% between 2013 and 2030, suppliers and end-users of electricity are seeking renewable sources of energy that include solar, wind, geothermal and tidal energy generation technologies.

Renewable energy systems have increased public awareness and have attracted both public and private investment around the planet. Political concerns about the continued supply of oil and natural gas, as well as scientific fears over global warming and the need to reduce carbon footprints from traditional power generation techniques have prompted widespread legislation based on specific goals outlined in the famous Kyoto Protocol (an international agreement on pollutants that calls for the reduction of greenhouse gases for the benefit of the future of the planet). This has created a significant increase in the number of national and local-level mandates regarding renewable energy systems and more importantly has created a significant increase in subsidies, especially for solar and wind generation forms of renewable energy.

For example, Germany, Italy, France and the United Kingdom, and Asian countries, such as China, India and Japan, have adopted Feed in Tariffs ("FIT") whereby the government pays between $0.30 to $0.40 per kilowatt hour over a 20-year time period for energy fed back into the utility grid. Also, in the United States, the federal government has offered tax incentives to spur the adoption of renewable energy. These incentives are intended to bring the production cost of electricity from renewable sources to be on par with power generated from fossil and other fuels, thereby encouraging creation of energy from clean and renewable sources. These incentives have proven effective in growing the renewable energy market around the planet, but have been, to date, most effective in Western Europe (Germany and Italy) which continues to account for the lion’s share of the global market for renewable energy systems and their respective sub-assemblies and components including capacitors.

IMF and the Global Economic Outlook: 2013

In its fall 2012 forecast, the International Monetary Fund (IMF) warned of the potential for a new global economic crash and has therefore reduced its forecasts for growth in the global economy for the second time in succession. The Fund is forecasting revised global growth rates of 3.3% and 3.6% for 2012 and 2013 respectively, which is 0.2 and 0.3 percentage points less than the forecast the IMF made in July 2012. The European debt crisis and the lack of economic growth in the U.S. are cited as the two primary reasons for the revised downward forecasts for the global economy. In the opinion of the IMF, the economy in the euro zone contracted by at least 0.4% in 2012 and will grow slightly, by 0.2%, in 2013. The IMF forecasts for Italy, Spain and Great Britain, were cut sharply. With regard to Germany, the International Monetary Fund expects gross domestic product (GDP) to grow by 0.9% in 2012 and 2013 because of the uncertain economic situation. The IMF still forecasts the strongest growth among the industrialized countries for the U.S. with growth rates of 2.2% for 2012 and 2.1% for 2013 but, at the same time, warns of the impact of unresolved fiscal problems in the U.S. The newly industrialized countries are likely to grow by around 5.3% on average this year and by around 5.6% in 2013. This is 0.3 and 0.2 percent points less than the forecast the IMF made in July. The IMF forecasts as well as the reality on the ground, have caused some governments to seriously reduce their feed-in tariffs for 2013, which is having the greatest affect on the European market for renewable energy systems. Major suppliers of inverters and aggregators of renewable energy technology have pointed to the reduced feed-in tariffs in Western Europe as the largest threat to market growth in 2013.

The Importance of the European Market for Renewable Energy Systems:

Europe accounted for almost 60% of global demand for renewable energy systems in 2012. Many European markets, in particular Germany and Italy, have adopted massive reductions in incentives in 2012 that will negatively impact the 2013 market. The cuts in the solar subsidy in Italy and Germany began to impact the renewable energy markets in the September 2012 quarter. Paumanok believes that demand in Europe will continue to fall sharply in 2013. At the same time, far greater price pressures are expected because comparatively large numbers of inverter manufacturers are competing in a smaller market.

The European Market and the Coming Changes in Feed-In Tariffs for Renewable Energy Systems

The European market has already been negatively affected by reductions in local government feed-in-tariffs and government subsidies in late 2012, with continued impact expected well into 2013. Changes in feed-in tariff incentives have negatively influenced customer demand for solar and wind renewable energy products in Europe. This in turn has created competitive pricing pressures that negatively impacted the revenue and profitability of turnkey suppliers of wind and solar projects and the components consumed in their manufacture. Paumanok believes that downward price pressure will have a negative effect on revenues throughout the renewable energy supply chain in 2013.

Italian Market Hard Hit by conto Energia V

For example, In Italy, the conto Energia V (Renewable Energy Act), which will probably be valid until the end of the first half of 2013, came into effect in August 2012. Compared with conto Energia IV, the feed-in tariff for power from solar energy plants was reduced significantly and annual new solar plant installations limited to between 1 GW and 2 GW for 2013 (compared to > 8 GW in 2011).

Changes in the German Renewable Energy Sources Act (EEG).

In Germany, too, at the end of June 2012 the Mediation committee reached an agreement about the future design of support for solar energy installations within the framework of the German Renewable Energy Sources Act (EEG). For small and medium scale solar power rooftop systems, the originally planned subsidy cuts were softened, while in the large-scale plant segment the deadlines for subsidy adjustments of the end of June 2012 and the end of September 2012 were kept intact. The range of 2.5 GW to 3.5 GW annual new installations established in the EEG was also kept intact- compared to the 2011 installations which were > 7 GW). However, government incentive support is to stop entirely if a total installed photovoltaic capacity of 52 GW is reached. Paumanok believes that these limitations will have a negative impact on the German supply chain for renewable energy systems in 2013.

Renewable Energy Turnkey Manufacturers Focus on New and Emerging Markets: 2013

Feed-in-tariffs and other related government legislation will continue to drive the revenue levels of the global renewable energy market. And while Europe will experience a difficult economic climate in 2013, renewable energy equipment vendors will expand into high-growth markets such as China, Japan, India, Latin America, Thailand, Middle East and North America in 2013.

The U.S. and China Markets and Government Tax Incentive Programs

The renewable energy markets in North America and China accounted for around one-third of global demand at the end of 2012. 2013 growth in these regions can probably compensate for the fall in demand in Europe, especially now that the Production Tax Credit in the U.S. was re-instated for one more year and modified to make it easier to obtain the credit. The Chinese market is critical to creating increased demand to offset the expected loss in Europe. However it should be noted that The Chinese solar market is dominated by solar plants for the power station class and is, because of the particular government certification requirements and the tendering process, not accessible to all internationally active inverter manufacturers and their capacitor suppliers. Through this practice, China supports their local economy with respect to their own solar cell producers, wind turbine manufacturers, inverter suppliers and component vendors.

Production Tax Credit (PTC) Trends in the U.S.

The U.S. markets will also grow in 2013. The driving forces for this growth in demand are the tax concessions applicable nationally and the expansion targets for solar plants defined for each state. The vast majority of the North America market is attributable to large-scale solar plants.

The Production Tax Credit has been the primary incentive for wind energy and has been essential to the industry’s research and development. Wind Power development in the U.S. has shown a great dependence on the PTC. The wind industry has experienced growth during the years leading up to the expiration of the PTC and a dramatic decrease in installed wind capacity in years where the PTC has lapsed. In 2003, 1687 MW of capacity was installed leading up to a lapse of the PTC in 2004. In 2004, only 400 MW of capacity were installed in the United States. The United States Government extended the PTC by signing into law the American Recovery and Reinvestment Act of 2009 (H.R. 1). The Wind PTC was extended an additional two years, expiring at the end of 2012. There are several incentives that go along with a Wind Production Tax Credit. The PTC provides a 2.1 cent per kilowatt-hour benefit for the first ten years of a renewable energy facility's operation. A second incentive of PTC is provided so that wind developers can receive a 30% Investment Tax Credit (ITC) in place of the Production Tax Credit. This only applies if the projects are placed in service between 2009 and 2013. Vestas Wind reported a dramatic increase in orders to the United States in the second and third quarters of 2012 which were driven by the PTC expiration at the end of 2012. However, Vestas also reported a decline in wind power factory activity in the third quarter of 2012 as the PTC expiration drew closer. However in January 2013 the PTC was extended for one more year in the final version of the Fiscal Cliff package and in fact the ability for companies to obtain the credit was made easier. This should have a positive effect on the North America market for wind turbines in 2013 as utilities rush to start production on turbines to take advantage of the tax credit before the end of the year. It should also have a positive effect on the U.S. market for power film capacitors and EDLC supercapacitors consumed in wind turbine systems.

Pricing Trends in Growth Markets for 2013

Paumanok is also expecting price pressures to increase in the expanding regions of North America and China as many companies have the same expansion strategy to offset the declines in Europe in 2013 and all vendors plan on having a sizeable share of the American, Chinese and Indian markets by the end of 2013. It is our experience in such environments that price erosion can be substantial as a result of such transitions.

2013 Forecast Installation Trends in Solar and Wind Technology:

For 2013, a newly installed solar capacity of between 27 GW and 33 GW (2012: 31 GW to 34 GW) is predicted globally. Compared with 2012, when global installed solar capacity was between 31 and 33 GW, this would suggest only small growth in demand for solar energy in 2013.

The same situation exists for wind power generation, of which new additions accounted for an estimated 34 GW in 2012 (With installed global capacity now at 273 GW). 2013 forecasts are expected to be up by about 7% to 36 GW, but severe price pressure is expected.

Taking account of the price pressure expected, and even though volume may be up due to high installation rates in China, India, Japan and the Americas in 2013, the downward price pressure will cause limits on value growth in the supply chain, however the 2013 market is still expected to grow.

Renewable Energy Competition with Traditional Energy Resources:

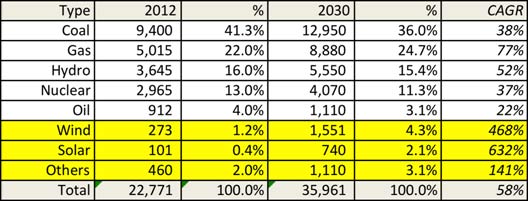

Based on a combination of data from Siemens AG and separate research from Paumanok Publications, Inc. for the 2012 year, we estimate that global installed capacity for electricity generation was 22,771 GW. This is expected to increase by 58% by 2030 to about 36,000 GW, which is a CAGR of 58%.

Installed Wind Capacity and Forecast Outlook to 2030

Based upon primary data, Paumanok estimates the global installed wind capacity in 2012 was 273 GW, up 34 GW from 2011. This represents only 1.2% of global electricity production. Paumanok estimates that wind power generation will increase to 4.3% of total electricity generation by 2030, or a CAGR of 468% between 2012 and 2030 when wind power is expected to be 1,551 GW of installed capacity.

Installed Solar Capacity and Forecast Outlook to 2030

Based upon primary data, Paumanok estimates the global installed solar capacity in 2012 was 101 GW, up 32 GW from 2011. This represents only 0.4% of global electricity production. Paumanok estimates that solar power generation will increase to 2.1% of total worldwide electricity generation by 2030, or a CAGR of 632% between 2012 and 2030 when solar power is expected to be 740 GW of installed capacity.

Therefore, after the market turbulence in 2012 and 2013 in the renewable energy market, the longer term outlook remains robust.

Figure 1: Renewable Energy Competition With Traditional Energy Resources (Electricity Generation by Type): 2012-2030 in GW

Source: Siemens AG Estimates, Forecasts Modified by Paumanok Publications, Inc. The reader will note how renewable energy resources represent only a fraction of the global energy output required. This supports the large projected growth rates for this technology to 2030. The long-term outlook for renewable energy systems is robust. “Other systems” noted above include tidal energy and geothermal, as well as other systems, both alternative and traditional.

Emerging Renewable Energy Technologies: 2013

During the course of Paumanok Publications, Inc. recent study on capacitor markets in renewable energy systems we were surprised to see the heightened level of activity in tidal energy equipment development worldwide (especially in Europe). This included new technologies designed to harness the energy of ocean wave technology, river currents and changes in the tides in harbors, bays and estuaries. The amount of new investment in the tidal energy sector, coupled with the increasing number of vendors of equipment in the space hinted at an emerging market with great future market potential. One of the most interesting aspects about tidal energy generation is that unlike solar and wind technology, tidal energy generation is not intermittent and is a steady source of renewable energy in comparison. The other segment of the market that is also generating interest is hydrothermal steam generation, although this technology offers the design engineer a number of challenges, not the least of which is that certain parts of the system require components to operate at as high as 300° C.

Capacitor Types Consumed in Renewable Energy Systems: FY 2013:

Based on primary research conducted for this report Paumanok has determined that there are three primary types of capacitors consumed in renewable energy systems. The reader should note that there are similarities between the circuits found in solar and wind renewable energy systems, primarily in the inverter and the DC link circuits that expand the overall market for capacitors consumed in this segment. Since long-term growth is expected for both wind and solar technology, the opportunity for capacitors is significant and should not go overlooked, especially by manufacturers of plastic film capacitors, aluminum electrolytic capacitors and double layer carbon supercapacitors.

Plastic Film Capacitors:

The largest renewable energy capacitor market by type is for the plastic film capacitor. The primary type of plastic film capacitor consumed in renewable energy systems is the polypropylene dielectric plastic film capacitor (PP or OPP), although the reader should understand that polyester type plastic film capacitors (PET) are also consumed, and that both polyethylene napthalate (PEN) and polyphenylene sulfide (PPS) dielectrics are also being considered for applications in renewable energy systems as well.

Polypropylene Plastic Film Capacitors

Plastic film capacitors have been traditionally used in power transmission and distribution applications for more than 100 years. They are excellent low cost capacitors for use in high voltage applications in the kilovolt range. They have been used by electric utilities for a long time because of the abundant nature of polypropylene (it is also used in soda bottles) which keeps its overall price low in comparison to many other dielectrics. However, the primary reason for its use from a technical aspect is that it is the only dielectric that offers self-healing technology, which means its reliability is excellent when subjected to high voltages in adverse conditions.

MKP Metalized Plastic Filtering Capacitors

From the German, MKP is translated, Metallisierter Kunststoff Polypropylen and is a specific type of plastic film capacitor manufactured from metallized polypropylene. MKP capacitors are used primarily for high AC voltages.

Most designs are large can, radial leaded boxed, or radial leaded with industrial strap terminals. Additional variations include radial leaded coated construction as well as axial leaded designs. The rated voltage is typically between 160 Volts to 3000 volts and the available capacitance range is generally between 0.00047 microfarads and 75 microfarads.

MKP capacitors are used as bypass, decoupling, DC link and smoothing capacitors. The capacitor acts as a low pass filter, preventing the transmission of AC voltages, suppressing fast transient changes and providing enough energy to the load. This circuit application requires that the capacitor have high resistance and low inductance.

MKP Capacitors are also used as Timing, Energy Storage and Ignition Capacitors, wherein the capacitor stores a charge until a specific amount of time (time delay) has elapsed. The capacitor stores a charge and then releases it in a short energetic pulse. This circuit application requires that the capacitor have good pulse characteristics.

MKP Capacitors are also used as snubber and resonant capacitors. In snubbering applications the capacitor protects semiconductors from over-voltages by high current switching. In resonant applications, the capacitor/inductor system oscillates at a certain frequency. This circuit application requires that the capacitor have good pulse characteristics and low Tan.

MKP Capacitors are also used in sample and hold circuits where the capacitor stores a voltage until a sample is taken. This application requires that the capacitor have a low rate of dielectric absorption.

MKP Capacitors are also used as EMI suppression components which requires a capacitor/resistor network on the input of a device that suppresses external noise pulses that could damage its components. This circuit application requires that the capacitor have a low degree of flammability.

MKP capacitors are also used in capacitor power supply circuits wherein the capacitor is used as a voltage divider without thermal losses. This circuit application requires the capacitor to have high capacitance stability.

In renewable energy systems such as wind, for example, MKP capacitors are used in the power conversion circuitry, primarily for the DC link circuit; for snubbering and filtering and in the inverter module. They are also used in the solar energy system for the exact same applications, but also have additional applications in the solar systems power supplies. MKP capacitors are also used in ocean wave generation power conversion circuitry as well.

MKV-Power Factor Correction Capacitors

MKV capacitors are based on a polypropylene dielectric and a paper strip with metal vapor-deposited layers on both sides alternating with plastic film. The paper is not located in the electric field but supports the vapor-deposited, regenerating aluminum metallization, the contact area of the metal end spray, and reduces the electrical field strength at the edges of the electrodes. The typical polymer-paper arrangement is processed in tubular capacitor windings which are subsequently vacuum impregnated with oil, without environmental or toxicological problems to ensure good heat dissipation from the winding to the surface of the case. This results in a long service life. Most of these capacitors are equipped with an overpressure dis-connector system. MKV capacitors have multiple applications, including commutating, general filtering, dampening, snubbering however, our interest with respect to their usage in renewable energy systems is for power factor correction.

Power factor correction is achieved using an MKV capacitor where there is high dv/dt, for tuned harmonic filtering and for applications with high thermal loading.

The rated voltages for such capacitors are usually between 400 and 800 volts, with capacitance values from 3 microfarads to 166 microfarads. Applications are in renewable energy motor drives and power conversion modules in both solar and wind energy systems. During the course of this study we noted a significant amount of these capacitors in large can configurations used for smoothing in the wind turbine inverters (14 per inverter). These are expensive capacitors, and their usage in such large numbers in wind turbine inverters is a lucrative segment of the renewable energy market worldwide.

Motor Run Capacitors/Geothermal

Motor run capacitors are AC voltage capacitors that allow the operation of asynchronous induction motors. The use of motor run capacitors increases the energy efficiency of motors and compressors by up to 12%. They also significantly improve the torque response of motors consumed in household appliances. This is particularly important for motors and compressors in continuous operation and thus applies especially to compressors in refrigerators and air-conditioning units. But motor run capacitors are also employed in a variety of motors that are consumed in other white goods, fans and circulators, office equipment, power tools and other household and professional end-products. Motor Run capacitors are designed for continuous duty, and they are energized the entire time the motor is running. For this report, we are interested in them motor run capacitors used in geothermal pumping motors. Most water pumping motors are split capacitor motors that require an AC film capacitor to operate. Primary sources reveal that such motors are used for geothermal pumping of water in geothermal energy systems.

Motor run capacitors are manufactured by winding metallized polypropylene on a mandrel and placing them into aluminum or plastic cans, or plastic boxes. Some motor run capacitors are radial leaded wrap and fill types, or ultra-small box type capacitors. During this study we also noted that some new designs are radically different from older versions and are more modularized in their construction. Regardless, every motor run capacitor we reviewed for this report uses thin metallized polypropylene as the dielectric material.

The majority of older type motor run capacitors use oil as a dielectric fluid and are considered wet constructions, while some are considered “dry” constructions because they employ a plastic resin as the dielectric fluid. The dielectric fluid is important because it aids in the transfer of ions between the dielectric layers and helps the finished capacitor achieve high voltages.

Not all vendors discuss whether or not they employ dry or wet constructions in their motor run capacitors, however, some of the leading vendors give us an indication of what type of dielectric fluids are employed. There is also an obvious move away from harmful chemicals and additives in dielectric fluids and a clear indication that vendors wish to displace their dielectric fluids with non-threatening organic solutions, or to move entirely too dry constructions when possible. We note that many key vendors now employ vegetable oils as their dielectric fluid of choice, with soybean oil and castor oil noted in the product literature. Dry type “fluids” are also quite prolific throughout the industry, with emphasis upon polyurethane dry resin. One major vendor, Regal Beloit, which sells the former GE brand capacitors, notes that their dielectric fluid is Dielektrol VI, a unique and proprietary formula which Regal Beloit believes gives them a competitive advantage over other vendors with respect to performance and live expectancy of the capacitor. Regal-Beloit is the only vendor of motor run capacitors who had a proprietary dielectric fluid in their capacitors.

The capacitance range for motor run capacitors generally runs from 1.0 microfarad to 100 microfarad, although there are some variations on this theme. Some vendors have lower capacitance values below 1 microfarad (such as 0.1 or 0.5) while other vendors have capacitance values that exceed 100 μF (some vendors have 120 μF, 180 μF or even 500 μF motor run capacitors, but these are limited offerings), the majority of products on the market rest between 1.0 and 100 μF. During this study we noted that there are 26 individual voltage ratings for motor run capacitors available on the market. Motor run capacitors will vary with respect to operating voltage based upon the region in which they are sold. We note that there are specific voltage products produced in the U.S. that differ from those produced in Germany or China, for example. However, there are some areas of overlap that need to be noted. Most vendors produce motor run capacitors in 250 VAC, 370 VAC, 400 VAC and 450 VAC. We note smaller product groupings in 500 VAC and 660 VAC, but these need to be noted as well.

Snubber Plastic Film Capacitors

As we have previously noted, MKP Capacitors are also used as snubber capacitors. In snubbering applications the capacitor protects semiconductors from over-voltages by high current switching. This circuit application n requires that the capacitor have good pulse characteristics and low Tan.

Snubber capacitors are also employed in renewable energy systems including solar, wind and geothermal for protection of the IGBT semiconductors.

Low inductance snubber capacitors are connected in parallel with GTO thyristors to limit the rate of rise of their repetitive reverse voltage. The voltage values are derived from their repetitive peak offstate voltage of the GTO thyristor. These capacitors are abruptly charged and discharged, whereby the peak value of the current reaches extremely high values. Extremely low inductance is important to the proper operation of snubber capacitors.

A variation of the snubber capacitor is the damping capacitor wherein AC capacitors are connected in parallel with semiconductor components to suppress or damp undesirable voltage spikes. Like the snubbers, damping capacitors are abruptly charged and discharged, the peak value of current that occurs being substantially greater than the rms figure. In addition to the sinusoidal halfwave voltage, damping capacitors carry periodic voltage peaks from the whole storage effect and harmonic components from phase controls.

Especially powerful GTO inverters for high-speed railway as well as industrial inverters call for special circuit designs to minimize switching losses. AC power capacitors especially designed for snubber applications keep switching losses to a minimum. Commutation of SCR devices is also considered a subset to the snubbing of IGBT power semiconductor devices. Commutating AC capacitors quench the conducting state in a semiconductor component. Commutating capacitors are generally subjected to high reactive power and peak current. Commutating capacitors must also be low inductance in design. The applications mentioned below can all be considered to be extensions of the variable speed drive market for asynchronous three phase variable drives. This represents the fastest growth portion of the power film capacitor market, with emphasis on snubber capacitors for protection of power semiconductors, which are the crucial component in variable speed drives.

DC Film Capacitors

DC film capacitors are manufactured primarily in radial leaded designs. These radial leaded designs are either molded box or dipped configurations. In a molded box, the film is wrapped around a core, placed in the box and the voids are then back-filled with epoxy. In the dipped design, the wrapped core is “dipped” in the epoxy. In surface mount designs the film is stacked in sheets and then extruded and chopped into capacitor case sizes. The volume of DC film capacitors sold are in the 5mm polyester film capacitor which is used in filtering circuits.

MKT Metallized Plastic Filtering Capacitors

From the German: (metallisierter kunststoff- or MKT polyester), a type of plastic-film capacitor. There are three primary markets for general purpose PET film capacitors; which are electrostatic capacitors used for bypass and decoupling; filtering and timing; blocking circuits and energy storage/discharge in the low to high voltage range; in capacitance values less than 10 µF. The primary markets for general purpose PET film capacitors are in (1) TV and PC monitors and in lighting ballasts. Other applications are diverse but center around (2) consumer electronic applications with emphasis upon consumer and car audio applications and in switchmode power supplies. The P5 Inductive GP PET film capacitors account for the majority of demand. MKT capacitors are also used in (3) DC link circuits and for general purpose filtering in power electronics, including in renewable energy applications such as solar and wind energy.

Interference Suppression Capacitors

International governing agencies such as Underwriter’s Labs (UL 1414 and 1283); Canadian Standards Association (CSA C22.2 No. 1 and No. 8); IEC (950 and 384-14) and European Community (EN60950 and EN32400) require that Radio Frequency Interference (RFI) that emanates from most electrical devices be limited to acceptable levels. The preferred method of limiting RFI is by incorporating a film or a ceramic capacitor in line-to-line and/or line-to-ground applications.

There are two main types of interference suppression capacitors, which are the X versions and the Y versions. These designations are the result of standards set by various international governing agencies mentioned in the introduction. In short, X capacitors are line-to-line capacitors used to suppress radio frequency interference in electrical systems; and the Y capacitors are line-to-ground capacitors used to suppress radio frequency interference in electrical systems. Interference suppression capacitors are employed in the inverters used in both solar and wind end-use renewable energy market segments.

Type X Capacitors:

Otherwise known as a line-to-line capacitor, these devices are used to suppress radio frequency interference (RFI) in electronic systems and are placed on the line between the main line and the neutral wires. X capacitors will generally have low capacitance values anywhere between 0.1 and 1.0 µF

Type Y Capacitors

Otherwise known as a line-to-ground capacitor; and is placed on the line leading from the main line to the chassis ground; or on the neutral line to the chassis ground. Y capacitors have small capacitance values to limit the 50 or 60 Hz leakage current to the ground. The 4700 pF type Y capacitor is a common value. Interference suppression capacitors are consumed in the power conversion circuits (inverter) of wind and solar energy systems.

Aluminum Electrolytic Capacitors

Aluminum electrolytic capacitors are constructed from two conducting aluminum foils, one of which is coated with an insulating oxide layer, and a paper spacer soaked in electrolyte. The foil insulated by the oxide layer is the anode while the liquid electrolyte and the second foil acts as the cathode. This stack is then rolled up, fitted with pin connectors and placed in a cylindrical aluminum casing. The two most popular geometries are axial leads coming from the center of each circular face of the cylinder, or two radial leads or lugs on one of the circular faces.

Large Can Screw Terminal Aluminum Capacitors

Large can aluminum electrolytic capacitors are consumed in renewable energy inverter applications for the DC link bus circuitry. These are generally high capacitance, high voltage, high ripple current and long life designs with rated voltages from 10 to 500 volts with capacitance values from 84 to 100,000 microfarads.

Snap Mount Aluminum Capacitors

The snap mount, or plug-in type aluminum electrolytic capacitor is also consumed in renewable energy systems, also for the DC link bus circuitry. These capacitors also have high ripple current, high capacitance and long life capabilities with rated voltages from 6.3 to 500 volts and capacitance values from 33 to 420,000 microfarad.

Carbon Supercapacitors

Also knows as Electric Double Layer Capacitors, or Supercapacitors - are alternative energy storage devices which store energy by electrostatically (physically) separating positive and negative charges. This is in contrast to batteries which store energy via orbital electron exchange (chemically). The lack of chemical reaction within permits ultracapacitors to be charged and discharged up to 1,000,000 times (compared to 100s or 1000s of charge/discharge cycles in batteries) - and at a faster rate than batteries.

Large Can Double Layer Carbon Capacitors

Ultracapacitors provide burst power for electric blade pitch control systems to ensure rotor speed remains within a safe operating range and/or optimize wind turbine output. The long life and maintenance-free capability make ultracapacitors the lowest lifecycle cost and most reliable power backup solution for pitch control systems. Pitch systems from 750KW to 6MW and up must be guaranteed to operate across broad temperature ranges and wind conditions. An added benefit is that the same ultracapacitor system can provide general backup power for the dc-dc link.

Double layer carbon supercapacitors are used in wind energy systems for pitch control of the turbine blades. Vendors usually sell wind aggregators specific modules composed of multiple 2.5 or 2.7 volt cells. These modules are usually 16 Volts, 75 Volts or custom cells with capacitance values from 58 to 500 FARADS. Primary customers in the wind energy sector have noted that there is great interest in expanding the role of the supercapacitor in renewable energy systems because of its green construction. Supercapacitors can be manufactured from organic materials to produce the activated carbon dielectrics and can employ water based electrolytes which is important to the end-customers driving demand for such systems.

There is also significant movement among solar energy system aggregators to use large-scale supercapacitor 560 volt reactive power modules for reactive energy storage and replace or augment batteries. Once again, the primary motivation behind this movement, according to primary vendors interviewed for this report is the green nature of the carbon capacitor which is non-toxic, lead free and whose carbon dielectric can be made from organic materials.

Summary and Conclusions:

Market opportunities exist for capacitors in established and emerging renewable energy systems in both the short and long term, especially for polypropylene (PP) film capacitors, polyethylene terephthalate (PET) film capacitors, large can screw terminal and snap mount aluminum electrolytic (Al203) capacitors, and for large can double layer carbon supercapacitors (EDLC). Key applications include power smoothing for solar and wind inverters, pitch and nacelle control for wind turbine blades and motor run capacitors for geothermal pumps. Short term opportunities will be challenging, with 2013 seeding a transition to regional opportunities in Asia, Americas and Middle East and away from the largest market in Western Europe due to mandated adjustments in tax incentives and tariffs. Global output for electricity from renewable sources such as solar, wind, tidal and geothermal energy should increase in 2013, but we expect that price erosion will accompany the transition to regional markets outside of Europe due to the large number of vendors in the supply chain and the apparent expectation that each one will garner significant market shares in China and the U.S. in 2013. The long-term opportunities to 2030 remain robust, with many countries around the planet creating specific goals for electricity generation from renewable sources ensuring significant growth opportunities for the equipment consumed in the production of wind, solar, tidal and geothermal energy systems.

Dennis M. Zogbi

Dennis M. Zogbi is the author of more than 260 market research reports on the worldwide electronic components industry. Specializing in capacitors, resistors, inductors and circuit protection component markets, technologies and opportunities; electronic materials including tantalum, ceramics, aluminum, plastics; palladium, ruthenium, nickel, copper, barium, titanium, activated carbon, and conductive polymers. Zogbi produces off-the-shelf market research reports through his wholly owned company, Paumanok Publications, Inc, as well as single client consulting, on-site presentations, due diligence for mergers and acquisitions, and he is the majority owner of Passive Component Industry Magazine LLC.