Thick Film Chip Resistors: A Mass Market in Turmoil

10/03/2017 //

Introduction

A current detailed analysis of the thick film chip resistor supply chain from raw material ores, engineered materials, substrates and pastes, unit production, distribution and consumption in each key product market reveals a market in turmoil entering the fourth quarter of CY 2017.

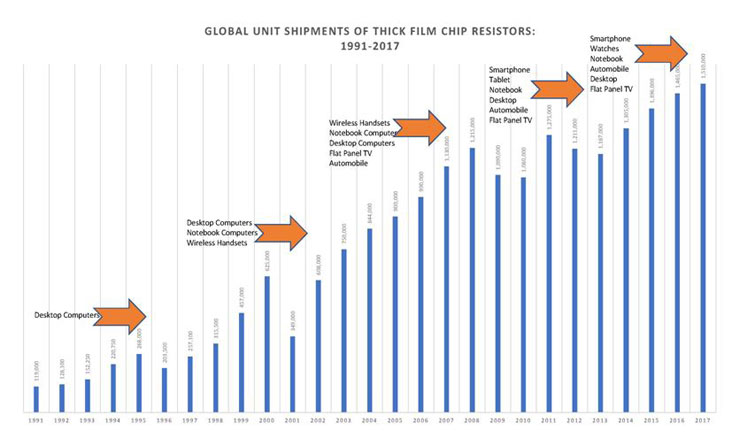

Global Consumption Volume for Thick Film Chip Resistors by Year: FY 1991-2017 (Paumanok Exclusive)

The following Figure illustrates our estimates for passive component “consumption” worldwide in terms of volume. To estimate the volume of global consumption for passive components we estimate the demand for end-products into which the passive components are consumed and how many passives per end-product arte required. In this manner, we also predict future demand. The following chart illustrates the historical increases in consumption volume for thick film chip resistors in conjunction with the related end-product that is consuming the majority of thick film chip resistor units worldwide. The summary of events is the introduction of computers, television sets and wireless handsets, each of which required an increasingly larger number of chip resistors per end-product, culminating in the “smart phone” which are thick film chip intensive.

Recent Changes in The Thick Film Chip Resistor Market and Reason for Review

A shortage of thick film chip resistors in the supply chain has motivated this release of this report. Global long-term customers of Paumanok in Japan, Korea and China know of the previous reports Paumanok has released on the subject of thick film chip resistors and has requested we do so again in FY 2017. To provide a benchmark by which manufacturers of substrates, metallization, components; and those that distribute and consume them in the electronic goods markets can understand current limitations and make accurate forecasts for the future, especially in expanding factories in Asia through an infusion of capital.

Figure 1: Thick Film Chip Resistor Consumption Volume (1991-2017)

Source: Paumanok Publications, Inc. In Millions of Pieces

Industry View of the Thick Film Chip Resistor in FY 2017

Inside the industry, resistors are viewed as a challenging market, especially for the mass-produced thick film chip resistor which requires significant economies of scale in production for the vendor to be successful.

Price competition is so intense that it’s difficult for vendors and distributors to make a profit in the highly intense and aggressive market that is based on the ability to produce extremely large quantities of individual parts. It is also difficult for resistor manufacturers to get financing for expansion given the limited return on investment and the expected slowdown in unit demand for parts given the saturation of the smartphone industry by global population

Technical and Industry Accepted Definition of Thick Film Chip

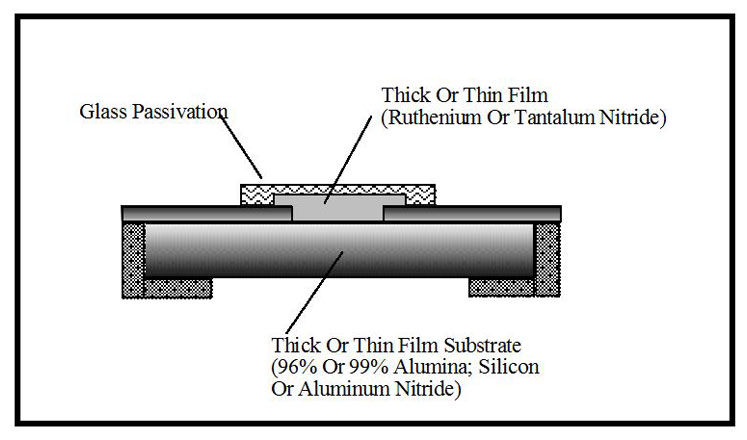

Thick film chip resistors are electronic components that provide resistance measured in ohms in all electronic devices, that are manufactured in specific chip resistor case sizes as designated by the industry, that have a 96% aluminum ceramic substrate, that have a ruthenium based thick film resistive layer with glass overcoat layer and precious metal terminations

Thick Film Chip Resistor Production Process

Different production processes for producing flat chip resistors are employed depending upon the type of chip resistor being produced. The majority of the world’s production of flat chip resistors involves screen printing of thick film mixed metals, which include primarily ruthenium oxide. Screen-printing produces layers as thick as 10 µm. The substrate material is primarily 96% alumina ceramic. In thick film resistors, the resistance value is determined by trimming, which is primarily accomplished using a CO2 laser, which is inexpensive and extremely fast. Terminations are applied to the fired resistors by either a dipping process, or through sputtering. Terminations for metal film resistors are almost exclusively sputtered; however, in thick film chips the terminations may be either dipped or sputtered. The end-terminations are then sometimes coated with lead-tin for improved wetting characteristics. The resistive surfaces are protected by glass passivity.

Illustration: Thick Film Chip Resistor

Figure 2: Thick Film Chip Resistor Schematic

Source: Dennis M. Zogbi Drawing

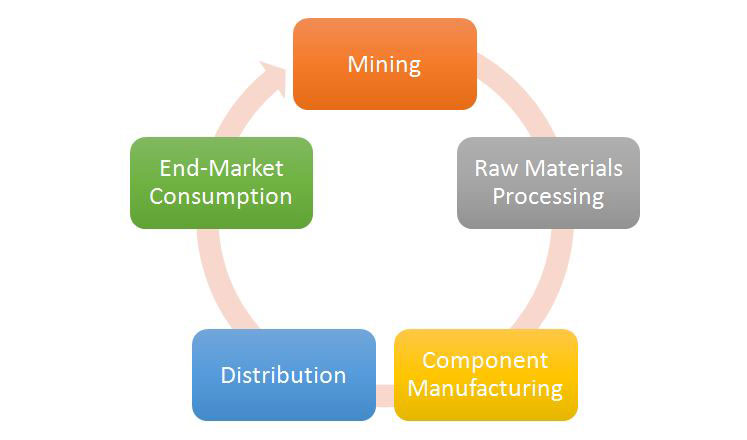

The Thick Film Chip Resistor Supply Chain:

Figure 1: The Passive Electronic Component Supply Chain

Source: Paumanok Publications, Inc. All Rights Reserved

An understanding of the passive electronic component supply chain is important in establishing a clear picture of the sub-sets of the global components markets. It is important for the reader to know that the supply chain begins in the ground as mined materials and ends in the recycling bin or the landfill.

Mining of Raw Materials

The supply chain for Thick Film Chip Resistors begins in the ground. Certain materials are critical to the production of electronic components and must be mined. These are all considered rare earths or rare metals to some degree, and there is always considerable competition for materials among industries and nations. In thick film chip resistors, the primary raw material that is mined is the alumina ceramic material consumed in the substrate. 96% alumina substrates are the primary substrate material consumed in thick film chip resistors because the ceramic material is extremely inexpensive. This is an important criterion for customers to understand, that the inexpensive nature of the raw material is directly proportional to the abundance of the material on Earth and its use in larger more stable industries. For Bauxite, the stability comes from the automobile and the aerospace industries, which consume aluminum in much larger quantities than electronics. This is a very good stabilizer of price for electronic components manufacturers and customers and should not be overlooked. The other variable is the key element in creation of the “thick film” is ruthenium, a platinum group metal (PGM) that is subject to dramatic fluctuations because it is absolutely dependent on the resistor industry as its primary customer AND its impacted by trading and speculation on its sister platinum group metals- palladium, platinum and rhodium. Changes in ruthenium price have and will continue to impact the bottom line of resistor manufacturers in the future and over the next five years.

Raw Materials Processing

Mined materials must be processed into usable forms to be processed into electronic components. Therefore, in all instances there is a chemical processing company that bridges the gap between the mine and the component manufacturer. In some instances, certain cost competitive passive component manufacturers have materials processing capabilities in-house. The engineering of raw materials requires an expertise in nanotechnology, or the ability to create consistent ultra-small shapes and patterns on which an electric charge can be manipulated. One of the primary maxims in component production is that the performance of the finished component is directly proportional to its size, or to its available surface area. This statement places great emphasis upon the importance of engineered raw materials. It also means that raw materials will have the largest price related to costs of goods sold. Companies in thick film engineering for the resistor industry provide readymade substrates according to EIA case sizes as processed from Bauxite and alumina powder; ruthenium oxide and ruthenium pyrchlore thick film inks, which require complex chemistry; and electronic glass passivation materials for component protection.

Component Manufacturing

Thick Film Chip Resistors can come in many EIA designated case sizes (shapes) and requires multiple disciplines to create. However, it can be said that in thick film chip resistors the basic form of manufacturing is screen printing of ceramic substrates with ruthenium ink (RU02). In many instances, there is the combination, or matching of materials in one element, and usually this is the combination of ceramic and metal (alumina and ru02 ink). Component production can also be viewed based upon “configuration.” Most capacitors are surface mount in configuration, however, a sizeable percentage of thick film chip resistors are the multichip array.

Component Distribution

Once a passive component is manufactured by a vendor, it must be distributed to the customer. Sales are either direct to an OEM (Original Equipment Manufacturer, otherwise known as a “brand” company- e.g. Intel, Samsung, Sony), or direct to an EMS (Electronic Manufacturing Services Company, e.g. SCI/Sanmina, Jabil, Foxxcon) or through an authorized distributor to serve the masses (TTI, Mouser). For direct sales to an OEM or EMS customer, the volumes must be of such massive proportions as to justify a dedicated sales channel. There are also cultural and regional differences. In the Americas and Europe, distributors now account for slightly more than half of regional sales, however, in the Asia-Pacific region, more sales are direct to OEM and EMS customers, regardless of size. However, even this is now changing to favor distributors.

End-Market Consumption

End-Market consumption of passive components can be viewed based upon the end-market into which the component is sold, and the region or country into which it is sold. The traditional product based end-markets into which components are sold include Consumer Audio and Video, Telecommunications, Computers and Peripherals, Automotive, Industrial and Specialty market segments. Within each category, specific products stand out, TV sets, wireless handsets, notebook computers and tablet computers, automobiles and power supplies each stand out as passive component intensive products that consume large quantities of capacitors per box. Automotive markets can be further broken down based on “Under-The-Hood” applications, and “Passenger Compartment” applications. The industrial market segment can be further broken down into power supplies, DC/DC converters, renewable energy systems, motors, fans and blowers, switchgear and switchboard applications, lighting and other line voltage equipment. Specialty markets can be broken down into defense and aerospace, medical electronics, undersea cable, mining electronics, railroad electronics, instrumentation and control equipment; seaborne electronics, and oil and gas services electronics (downhole pump).

Based upon world region, the Asia-Pacific region accounts for between 70% and 80% of all components consumed, with China and Japan the two largest consuming countries, but Korea, Singapore, Philippines, Thailand, Malaysia and Indonesia are also key countries that build larger assemblies that require passive components to operate. The Americas and Europe account for between 10% and 15% of consumption of components each; and key consuming countries are Germany, The USA, Mexico, Brazil, the Czech Republic, Hungary, UK, France and Italy.

When we began researching passive components in the late 1980s, the computer was the new product on the global market that began to compete with parts from the massive consumer audio and video imaging markets. During the past 30 years, the rise of the handset has dominated all other aspects of the high-tech economy and completed dictated the design and direction of the thick film chip resistor and will continue to do so over the next five years. Movement toward ultra-small components is more advanced in MLCC (capacitors) and thick film chip resistor manufacturers must make investments to produce the next generation of ultra-small passive component to satisfy growing markets in handset modules and smart watches. Additional shifts in technology, including the movement from cathode ray tube to flat panel display; and the continued “electronification” of the automobile; with additional breakthroughs in medical implant technology, oil and gas electronics, renewable energy systems, data storage and space exploration occurring along the way and giving valuable opportunities to component vendors like you who spend the time and read market research and prepare for the future.

Recycling of Critical Materials

The final part of the supply chain for components is recycling. Many products are recycled to reclaim their precious and rare metals, and recycling also occurs at various stages of the supply chain. The primary products that are reclaimed include ceramic capacitors, tantalum capacitors and resistors, and the primary targeted metals for recycling include palladium, gold, ruthenium, silver and tantalum. Other materials such as nickel, copper, aluminum and plastic are not recycled to any great degree because they have limited value. However, we do know firsthand of companies extracting ruthenium from thick film chip resistors, especially when there is a shortage of thick film chip resistors and the price of ruthenium spikes or skyrockets as it has done repeatedly in the past 30 years.

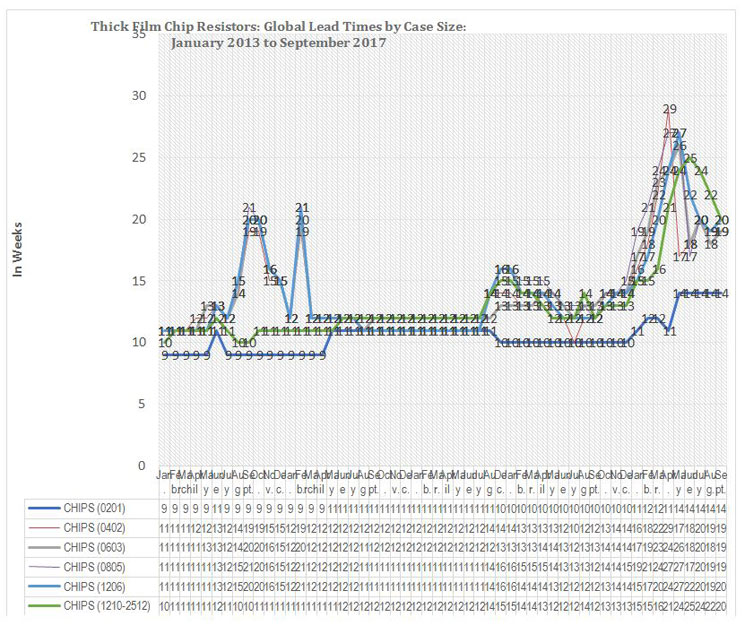

Resistor Lead Time Trends: FY 2013-2017 by Month and by Case Size from 2013 to 2017 (55 Months of Lead Time Data for Thick Film Chip Resistors

The thick film chip resistor lead times showed increased demand again in September 2017 especially for the larger case size parts in the 0603 and 1206 case sizes suggesting strong demand from the wireless handset, computer and automotive industries respectively.

Figure 4: Thick Film Chip Resistors: Lead Time Trends in Weekes by Case Size: January 2013 to September 2017

Source:Paumanok Publications, Inc. Monthly Lead Time Index for Passive Electronic Component

Understanding The Current Global Economic Environment

Global Economic Conditions and Outlook to 2022

The global economy in the 2017 fiscal year once again reflected the change in currency having direct influence on the passive component industry. As we had forecasted, the global economic pendulum “swung the other way,” due to the raising of interest rates in the United States. This created greater value in US dollars for passive components as noted in this study, while those vendors reporting in yen and won experienced a slowdown and those reporting in New Taiwan $ and Ruan continued also to grow.

Current Shortages of Passive Components: Especially Thick Film Chip Resistor Prompts This Report

Shortages exist at this writing for thick film chip resistors of all types and for all applications as is shown in detail in this report through primary and secondary information and deep data rick resource application as only Paumanok can provide.

The current shortages in thick film chip resistors came AFTER shortages emerged in surface mount capacitors as is described here- Shortages in High Capacitance MLCC and Tantalum Chip Capacitors were parlayed into shortages in almost all other surface mount components with Thick Film Chip Resistors emerging as the one of the most difficult components to find in 2017. Prices have also increased by 15%. However, as many seasoned veterans of the electronics industry know, these areas of asymmetrical highs in the industry are soon followed by dramatic drop offs in demand as the pendulum swings the other way. Thick film chip resistor manufacturers may find comfort in knowing that capacitor manufacturers feel that pressure will remain on in MLCC for 15 months. However, it is Paumanok’s experience that competition, especially in Asia (ie. Korea, Japan, China) usually speeds up the technical advancement and capacity expansion in the component industry. The intense nature of the competition and national pride among the three countries still making these parts in any great volumes – China, Japan and Korea, will certainly keep pressure to compete through the addition of massive economies of scale an imminent reality- too many vendors with significant financial resources coming from both public and private equity, investing in resistors because of their UBIQUITIOUS and NECESSARY position in the global high-tech economy.

Positive Market Indicators

The positive influences on the market are as follows –

- The computer market grew 10% in value for passive components in FY 2017 due to the weakening of the dollar to the yen during the year. Computer manufacturers had to pay more for components in FY 2017 while their volumes continued to decline.

- The automotive market was up 8% in value for passive components in FY 2017 due to the weakening of the yen to the US dollar. A weak dollar favors the auto and computer sectors.

Negative Market Indicators

The negative influences on the market are as follows –

- The Industrial and Power end markets were stagnant in FY 2017

- The Consumer AV markets were stagnant in FY 2017 and still under significant downward pressure due to continued encroachment of their product markets by handsets.

- The Specialty markets were pulled down by the drop-in oil and gas electronics spending, but were pushed up by sales for aerospace and optical networking.

- AND passive component revenues from the handset business dropped 2% in 2017.

Overall Outlook to 2022

Our long terms forecasts for market recovery for passive components in this report suggest that this will begin in Fiscal year 2017, and persist through 2022.

Changing View on Passive Component Unit Sales to 2022

- Our view continues to be that of a slower growth requirement for mass produced high volume piece

- Thick Film Chip Resistors included

Key Findings of this Report:

- Thick Film Chip resistor revenues from the wireless handset market declined for the first time in recent memory, signifying a trend toward slower growth rates coming from the telecom sector than in previous decades.

- Regardless, thick film chip resistor shortages reached a high point in the September quarter of 2017, with shortages building all year as is evident in the lead time data included in this report.

- The computer market is seeing a revival in dollars and this is driving up demand for thick film chip resistors and there is not enough capacity to handle this so passive component shortages abound in 2017. However, this is different from previous shortages such as the one that occurred in 2000 which were materials related. This shortage is due to a bottleneck in capacitor supply in large case size chips for the computer markets and the automotive markets which is bleeding into other sectors, most notably thick film chip resistors.

- Automotive continues to improve if not so much for unit sales, which should slow to 1% next in volume output, but will also increase in content per vehicle so we still see more growth in automotive sector over the next five years and the continuation of other specific markets.

- The oil and gas electronics have dropped by 50% and have put a strain on the high temperature and high voltage capacitor markets. But this should begin to change in 2018 and start to recover.

- Space electronics continue to drive demand for specialty passive components, including a nice increase in demand for mixed metal oxide supercapacitors for pulsed data transmission from satellites.

- Medical implant components are also a good growth market, while test and scan equipment have shown a slowdown, but should increase with an improving global economy.

- Optical networking equipment and wireless base stations still provide a good growth platform for extending value-added and application specific thick film components.

Dennis M. Zogbi

Dennis M. Zogbi is the author of more than 260 market research reports on the worldwide electronic components industry. Specializing in capacitors, resistors, inductors and circuit protection component markets, technologies and opportunities; electronic materials including tantalum, ceramics, aluminum, plastics; palladium, ruthenium, nickel, copper, barium, titanium, activated carbon, and conductive polymers. Zogbi produces off-the-shelf market research reports through his wholly owned company, Paumanok Publications, Inc, as well as single client consulting, on-site presentations, due diligence for mergers and acquisitions, and he is the majority owner of Passive Component Industry Magazine LLC.